- Corn ½ lower to 1 ¾ higher

- Soybeans 9 ¼ to 6 higher

- Wheat 2 ¼ to 2 ¾ higher

- Basis Flat/Higher

- Live Cattle 208 higher (250.10)

- Dow Jones 713 lower (50,185)

- Crude Oil 197 higher (90.15)

- Feeder Cattle 23 higher (354.38)

If modest bounces count as a winning day, then today qualifies. With increased bombing and tensions between the US and Iran driving world equity markets sharply lower and crude oil higher, our markets bounced modestly on positioning ahead of Thursday’s June USDA monthly report. Fundamental grain and soy news leans bearish as China still has shown no initiative to further open their markets to the US while US weather is wet, but potentially overly so. If Thursday’s USDA report is a non-event, the markets will continue to be pushed and pulled by news from Iran.

News and Notes:

- The next week looks wet and turning cool, which is not what many need. The US growing season mantra of “Rain makes grain” has been around forever, but there are many areas of Corn Belt where they are not getting gentle rains, but torrential downpours adding up to 6”+ in a couple of days. It is very hard to track replanted acreage, but the increasing areas that have too much water need to be considered. How many corn acres will be shifting to beans? How much fertilizer has leached out? These weather-related considerations are not currently priced in the market.

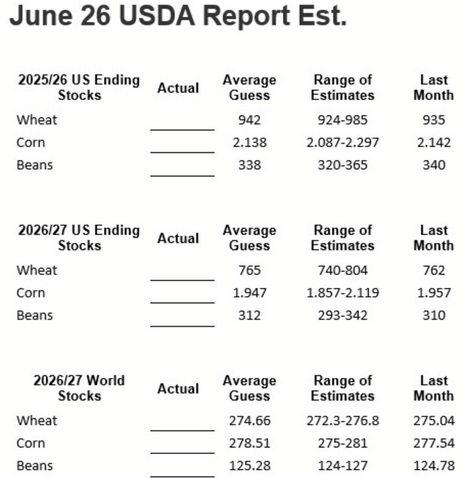

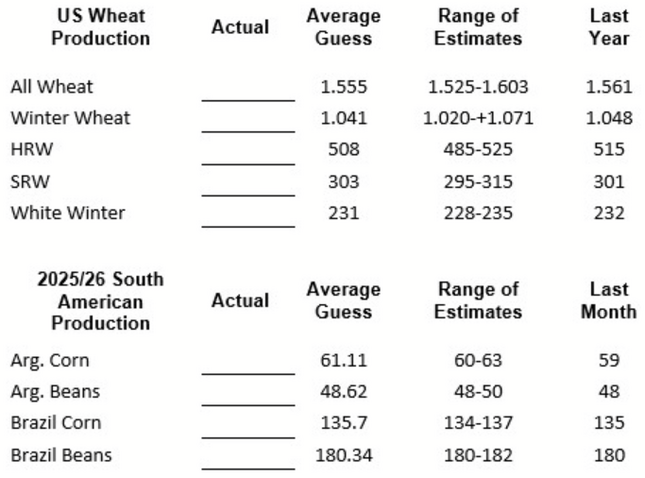

- The estimates for Thursday’s June USDA monthly update are on Page 2 and show the multiple columns where the USDA and WASDE will offer updates. The report will be released at 11 central but is not expected to be a major market mover but two variables are a larger cut to the US wheat crop and where WASDE will predict SA yields. There will not be a US acreage or yield update until the massively important June 30th Quarterly Stocks and Acreage Report.

- The war with Iran is escalating against as the US retaliated for Iran shooting down a US helicopter and then Iran began firing missiles on their neighbors in the Middle East and other targets. President Trump’s thoughts that negotiations are going well but we’ll bomb the hell out them if we have to is not what any of the markets want to hear. Before the recent corn and bean break, higher crude oil would always pull corn higher. That is no longer the case as crude was up sharply while corn was flat. More frustration is discovered every day, rather than less.

- There were no daily flash sales announcements and Thursday’s weekly sales totals are not expected to be very impressive. If China is going to start bargain shopping to get their trade deal promises started, they are going to have to lower or eliminate their 10% tariff on US imports and there are no rumors that will happen soon. One international piece of positive demand news is Brazil is likely to pass a measure increase their ethanol production within the next 2-weeks. The more corn Brazil uses, the less they will have to sell to China.

The daily news flow continues to be a short list of repeating headlines which will not change anytime soon. The market needs to hear China is moving toward buying the extra US bushels promised during last month’s trade meeting as we inch toward the market reset that normally comes with the June 30th acreage and yield numbers. Tomorrow’s USDA report comes out at 11 and I will put out an overview of the report and the overnight and morning news shortly after.

Sales Targets

Corn

Beans

Wheat

- 2025 Crop Finished Finished Finished

- 100% Sold at $4.48 Avg 100% Sold at $10.67 100% Sold at $6.24 Avg

- 2026 Crop On Hold - Dec ‘26 On Hold – Nov ‘26 On Hold– July ‘26

- 60% Sold at $4.78 50% Sold at $11.05 65% Sold at $6.24

- Current Price $4.47 $11.39 $5.88

- 2027 Crop On Hold - Dec ‘27 On Hold – Nov ‘27 On Hold– July ‘27

- No Sales Yet 10% Sold at $11.50 25% Sold at $7.15

- Current Price $4.76 $11.23 $6.49

%’s are total of expected yields. Bold Prices are Updated Sales Targets. * price includes trading

Today’s Market Closes — Rounded to the Nearest Cent

Corn

- July $4.19

- September $4.28

- December $4.47

- March $4.62

Beans

- July $11.23

- September $11.26

- November $11.39

- January $11.52

Wheat

- July $5.88

- September $6.00

- December $6.17

- March $6.33

Other Closes

- August Diesel 3.5768 +591

- Dec Cotton 75.30 unch

- Cash Cattle $260 Offer

- Lean Hogs 93.18 -40

Any decision to purchase or sell as a result of the opinions expressed in this report will be the full responsibility of the person authorizing such transaction. No market data or other information is warranted by Reliance Capital Markets II LLC as to completeness or accuracy, express or implied, and is subject to change without notice. Any comments or statements made herein do not necessarily reflect those of Reliance Capital Markets II LLC, or their respective subsidiaries, affiliates, officers or employees. Disclaimer: Past performance is not indicative of future results. Strategic Trading Advisors is a registered DBA of Reliance Capital Markets ll LLC.

About Jody Lawrence

Jody Lawrence has been in the commodity brokerage and agriculture marketing business since 1992 and started Strategic Trading Advisors in 1999 and runs it today with his son Brady. The daily market comment his company publishes has over 7000 subscribers in 33 states and 3 countries and provides a concise overview of the world markets with ideas on farm hedging and marketing. Jody also travels the country giving 60-70 marketing meetings a year through his 22-year strategic partnership with Helena Agri-Enterprises.

About Brady Lawrence

Brady Lawrence is an Agriculture Market Specialist and Financial Advisor that focuses on commodities markets, futures and options brokerage, and helping individuals and families plan for retirement and their financial futures. Brady joined Jody at Strategic Trading Advisors in 2018 after college and supports the market research and brokerage sides of the business.