- Corn 3 ½ to 4 ¼ lower

- Soybeans 10 to 13 ½ lower

- Wheat 9 ½ to 12 higher

- Basis Flat/Higher

- Live Cattle 238 lower (235.25)

- Dow Jones 137 higher (52,761)

- Crude Oil 144 lower (72.08)

- Feeder Cattle 590 lower (356.15)

The corn and bean markets took a breather today and finished modesty lower as both fell back to fundamental support ahead of Friday’s USDA report. The losses make it look like the forecasts turned cooler and wetter, but they remain stressful in the short-term with a return of more heat next week. Wheat had the best day of the three major markets as end users purchased yesterday’s break expecting another cut to the US’s crop in Friday’s report and the substantial crop loss in Europe. The weekly export report was nothing too impressive, but a morning confirmation of the second Chinese bean purchase was part of the daily sales report. Crude oil was initially higher but ended the day lower as the world markets are continuing to only pay short-term attention to the developments in Iran despite more overnight bombing by the US. Chinese demand news, US weather forecasts interrupted briefly by tomorrow’s report will be the drivers into the end of the week.

News and Notes:

- The mid-day forecast continues to keep heat in the far WCB and S Plains for the next 4-6-days, but the major forecast models remain at odds about the intensity of the upcoming heat and how far east the dome may move. In a week, more rain will be needed for the entirety of the Corn Belt. NOAA released their historical data on June this week and June combined to one of the wettest and warmest in the 131-years of their record keeping. Super El Nino is still expected to be in place soon.

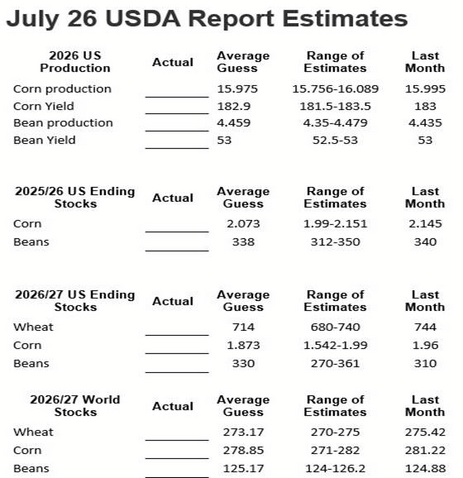

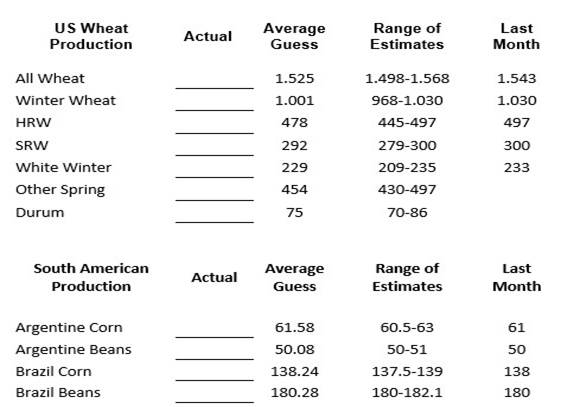

- The lengthy list of the columns expected to be adjusted in Friday’s USDA July report is on Page 2 with all major domestic and world numbers to be addressed. The planted acreage changes from the June 30th acreage report will be included, but the wild card is if the USDA gets aggressive to do much with BPA yield considering the inconsistent US weather to this point. If the report is a non-event, attention will immediately turn back to US weather forecasts and Chinese demand updates. The report will be out at 11 a cst.

- The USDA weekly export sales report held no surprises and there were no industry rumors of additional Chinese interest today. How the USDA addresses the May trade deal with China and promises of additional corn and bean purchases will be an interesting footnote to look for in the report.

- The cattle markets have been extremely volatile this week on a lack of any major news about screwworm or other big market movers. The daily feeder cattle ranges have average $7 for the week.

- President Trump said that Iran wants to make a deal after the US targeted bombing of the last few days, but the world markets have only added back $5-$7 of Straits closure premium while the world equity markets are shrugging off this week’s events and posting weekly gains to this point.

With no market moving updates on demand or US forecasts that moved the markets, the list of things to write about is short. The biggest potential adjustment I will be monitoring in Friday’s report is the direction of any USDA yield change. It is unlikely they will touch bean yield, but any reduction, even half a bushel lower would set up an interesting reaction from the trade as crop ratings continue to decline and are now well below last year’s record yield. We will put out a post-report update tomorrow and hopefully have bullish news to discuss and higher markets.

Sales Targets

Corn

Beans

Wheat

- 2025 Crop Finished Finished Finished

- 100% Sold at $4.48 Avg 100% Sold at $10.67 100% Sold at $6.24 Avg

- 2026 Crop On Hold - Dec ‘26 On Hold – Nov ‘26 On Hold – Sep ‘26

- 60% Sold at $4.78* 50% Sold at $11.05 65% Sold at $6.24

- Current Price $4.52 $11.82 $6.20

- 2027 Crop On Hold - Dec ‘27 On Hold – Nov ‘27 On Hold – July ‘27

- No Sales Yet 10% Sold at $11.50 25% Sold at $7.15

- Current Price $4.79 $11.60 $6.57

%’s are total of expected yields. Bold Prices are Updated Sales Targets. * price includes trading

Today’s Market Closes — Rounded to the Nearest Cent

Corn

- July $4.28

- September $4.32

- December $4.52

- March $4.67

Beans

- July $11.80

- September $11.70

- November $11.82

- January $11.96

Wheat

- July $6.11

- September $6.20

- December $6.34

- March $6.47

Other Closes

- August Diesel 3.5716 -859

- Dec Cotton 80.63 -4

- Cash Cattle $260 Offer

- Lean Hogs 98.15 -150

Any decision to purchase or sell as a result of the opinions expressed in this report will be the full responsibility of the person authorizing such transaction. No market data or other information is warranted by Reliance Capital Markets II LLC as to completeness or accuracy, express or implied, and is subject to change without notice. Any comments or statements made herein do not necessarily reflect those of Reliance Capital Markets II LLC, or their respective subsidiaries, affiliates, officers or employees. Disclaimer: Past performance is not indicative of future results. Strategic Trading Advisors is a registered DBA of Reliance Capital Markets ll LLC.

About Jody Lawrence

Jody Lawrence has been in the commodity brokerage and agriculture marketing business since 1992 and started Strategic Trading Advisors in 1999 and runs it today with his son Brady. The daily market comment his company publishes has over 7000 subscribers in 33 states and 3 countries and provides a concise overview of the world markets with ideas on farm hedging and marketing. Jody also travels the country giving 60-70 marketing meetings a year through his 22-year strategic partnership with Helena Agri-Enterprises.

About Brady Lawrence

Brady Lawrence is an Agriculture Market Specialist and Financial Advisor that focuses on commodities markets, futures and options brokerage, and helping individuals and families plan for retirement and their financial futures. Brady joined Jody at Strategic Trading Advisors in 2018 after college and supports the market research and brokerage sides of the business.